Cryptocurrency was created in great part to provide a way to escape currency debasement and unpredictable monetary policies. Satoshi put it clearly:

“The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust.”

This is why it’s crucial for any cryptocurrency to:

-

Set a monetary policy that isn’t debasing by itself (so it should target low, zero, or negative inflation).

-

It’s set in stone, so no trust on influential entities (foundations, core developer teams, big holders, etc) is required.

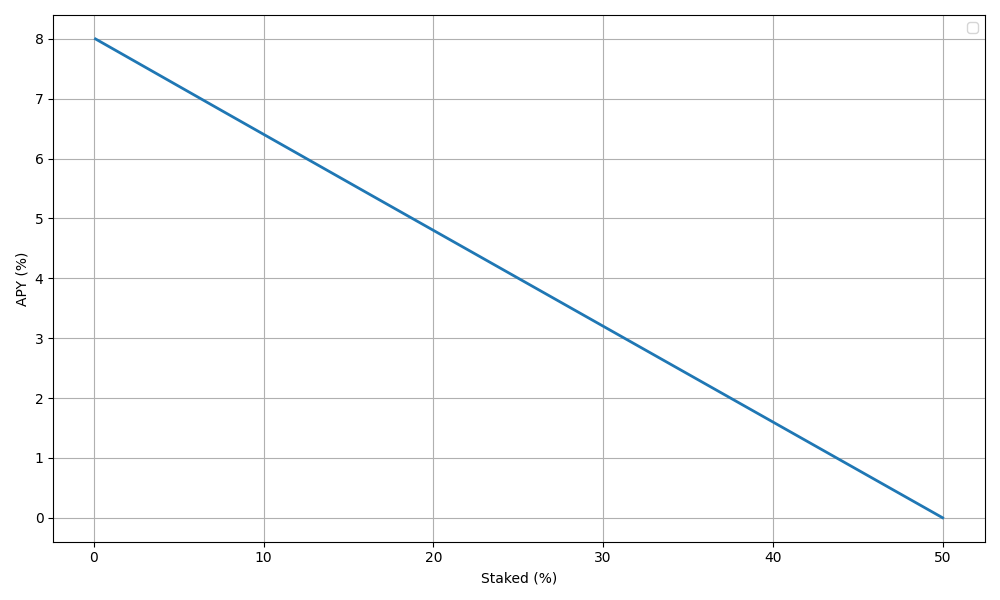

High inflation may look like a good way to incentivize people to participate in the network by staking and delegating to avoid getting diluted, but this hurts distribution and economic participation.

A highly inflationary policy is too much overhead for most holders, which in some cases can’t even get yield, like in the case of ETFs or other financial vehicles, prevented by law, fiscal inefficiency, operational complexity, etc. The same goes for liquidity providers which can’t provide liquidity and stake at the same time; traders opening positions on exchanges; and all kinds of economic actors and activities being negatively impacted by being in situations where they can’t stake their MINA or doing so represents operational friction, capital inefficiency, or simple inconvenience. Not to mention the psychological effect of poor price performance, even if the yield makes up for it.

This also severely damages the prospects of MINA eventually becoming a unit of account, given that denominating prices, salaries, contracts, or other economic mechanisms in MINA becomes more complex by having to account for the high inflation on top of volatility.

Some could suggest that this will be solved through liquid staking, but then the initial motivation of high inflation to incentivize people to participate directly in staking and delegation is completely negated, providing only great disadvantages to MINA.

This may not seem relevant in the early stages, since high volatility dominates due to relatively small volume and valuation, but it preemptively puts MINA at a disadvantage in its path to become a world currency, which is what it should strive for.

Over the years a trend emerged where people increasingly focused on chain activity as a result of focusing on chain revenue gained through transaction fees. A trend that can specially be tracked back to when Ethereum was trying to distinguish itself from Bitcoin and branding itself as “digital oil” in contrast to Bitcoin’s “digital gold / money / store of value”. Changing the focus from decentralized money to block space demand and transaction volume; arguing that decentralization trade offs like increasing requirements to run a node, were justified to increase the usability of the chain, which in turn would provide more value than a more decentralized but lower usability and throughput chain like Bitcoin. Similarly, Ethereum also dismissed criticism about the uncertainty around its monetary policy.

Eventually Ethereum realized that this was a mistake, since changing the focus from decentralized money to “chain revenue” quickly became a race to the bottom on decentralization to increase usability and revenue from transaction fees. Eroding the value accrual that comes from being a candidate to become a world currency by offering a store of value on a platform with high decentralization, censorship-resistance, and liveness; and being valued more in terms of a tech company with chain revenue and user growth at its center.

Ethereum realizing its mistake then took the steps to pivot from being “digital oil” to “ultrasound money”, refocusing on how it was more decentralized than new chains with faster and cheaper transactions and strengthening the confidence of its monetary policy by reducing inflation and showing more commitment to stick with it.

The issue is that despite all of these changes to become “ultrasound money”, Ethereum wasn’t able to get rid of the chain revenue narrative, combined with the fact that attached to the “ultrasound money” strategy was the hype around how fee burning would turn ETH into not only a currency with low inflation, but a deflationary currency. Cementing the focus on chain revenue.

This environment has resulted in Ethereum losing market share in the “digital money” category against Bitcoin and losing market share in the “digital oil” category against chains that make even greater decentralization tradeoffs but increase chain revenue and user growth like Solana.

Meanwhile Mina is one of the few blockchains that isn’t compromising decentralization and has an architecture that could eventually surpass even Bitcoin’s decentralization. Therefore Mina should aim to compete with Bitcoin on the world currency stage.

Of course this doesn’t mean that Mina should disregard the importance of chain usability. A chain with active block space demand is a healthy indicator and Mina is trying to be more than decentralized money. It is creating a cryptographic platform for zkApps which not only enable traditional smart contract use cases but also new ones. In fact, Mina has been focusing more on the latter and that’s why this is a call to increase focus on Mina to establish a solid decentralized money identity, which is fundamental to distinguish Mina from all the other smart contract platforms, taking advantage of its unique and innovative architecture. Avoiding falling in the trap of focusing on how to increase chain revenue over its natural edge to become a global reserve currency, just like Bitcoin, which doesn’t derive its value from chain revenue. Mina needs to aim for being the same. Chain revenue doesn’t even equal value for users and can be the opposite, as exorbitant fees from sandwich attacks and other forms of MEV providing high chain revenue demonstrate. So Mina should focus on becoming the most decentralized platform in the world, providing the best place for people to store their money, through unmatched node count, liveness, censorship-resistance, and verifiability thanks to its succinct architecture; combined with a rich and composable zkApp ecosystem that allows users to do many more things natively with their MINA that isn’t possible to do natively with BTC (like a zkApp for payments that is more efficient and easier to use than the Lighting Network; native swaps, lending, stablecoins, etc). MINA can accrue a lot of value by focusing on these properties and functionalities even if the chain revenue is relatively low, which wouldn’t even be surprising, given that in Mina a single zkApp or L2 transaction could contain millions of transactions for that zkApp or L2, which Mina will happily verify fast and inexpensively.

Mina could choose to do things like burning fees, but that should never be a distraction from the real goal. Mina should be above anything else decentralized money that protects people from currency debasement and uncertain monetary policies. Just like Bitcoin. Although even Bitcoin has the issue of chain revenue being a concern, since its long term security depends on how much fees users pay to miners. It’s just that this concern has been pushed to the future by subsidizing security through a temporal period of diminishing block rewards. To avoid this, the main source of revenue for validators should be a perpetual subsidy of security through block rewards that result in low inflation. Paying 7% yearly of the whole supply is too taxing due to the previously discussed reasons. Setting a low inflation target could even result in a higher budget for security, given that a greater value accrual would translate on validators being paid with a more valuable asset even if the amount is nominally lower (e.g. 1% of a $100 billion valuation is 1 billion, which is a bigger budget than $70 million from 7% of a $1 billion valuation).

Establishing MINA as decentralized money is critical to trigger a virtuous cycle of people being more willing to keep their money in Mina, increasing economic activity, security, user growth and retention; improving the composability between native zkApps and the incentives to deploy on Mina, which would improve the user experience, attracting even more holders and users and so on.

Once it is clear that we want to establish a predictable monetary policy with low inflation, the next question is what this monetary policy should be. Bitcoin and Ethereum are the top 2 most successful cryptocurrencies by a big lead, and arguably the most perceived as money-like in general, with Bitcoin dominating due to the reasons already discussed. Still Ethereum is a formidable project based on a lot of research and that has a Proof of Stake (PoS) issuance model that so far has proven to be effective to secure a blockchain worth hundreds of billions of USD, including perpetual issuance to subsidy the security of the blockchain and avoid the potential of ending on a situation where the budget to secure the blockchain is too small relative to the valuation of its total native cryptocurrency.

Currently Bitcoin’s issuance is slightly higher than Ethereum:

The formula to calculate yearly ETH issuance is:

Where N is the number of validators with 32 ETH operating in optimal conditions, which results in a theoretical max inflation of around 1.5% yearly if all the ETH at the moment of writing was staked. Current number of validators is around 1,054,000, resulting in an issuance of around 965,274 ETH per year, and with a current ETH circulating supply of around 120,514,017, this equals an issuance of around 0.8009%.

So at the moment of writing, Bitcoin and Ethereum have a similar budget of around 0.8% of the native value they are securing, showing no issues so far with this security budget and demonstrating that this level of inflation is attractive enough for people to consider BTC and ETH as financial vehicles to escape from the debasement of fiat currencies or as a form of investment. Making an issuance target of around 0.8% a reasonable target for Mina going forward.

Now the remaining question is how Mina should approach such an issuance target. Given that Mina follows a more elegant and simpler consensus algorithm than Ethereum that doesn’t rely on attestations, sync committees, or slashing, we could simply change the target inflation to 1% in a future hard fork. Setting MINA free to be used in all kinds of economic activity without worrying too much about dilution and priming it for becoming the most decentralized store of value. With validators being rewarded for securing the blockchain in a cryptocurrency better designed to increase its economy, accrue value, and reduce volatility and uncertainty.

Naturally this should be carefully discussed and this only pretends to kickstart the discussion, gauge community sentiment, and gather feedback to create a solid MIP. It’s extremely important that something like this has broad support and is set on stone, since we probably have only one shot at changing Mina’s monetary policy. Otherwise, further changes could severely damage its credibility as a reliable monetary policy.